Disclaimer: Opinions expressed below belong solely to the author.

Here’s some good news for borrowers. According to the latest report by Bloomberg, banks in Singapore are so flushed with cash from deposits pouring into the city-state that they no longer know what to do with it.

This forced the country’s largest bank, DBS, to offload S$30 billion to the Monetary Authority of Singapore (MAS), as admitted by CEO Piyush Gupta during an analyst call (transcript here) last month.

We are not finding enough opportunities to put the money to work and instead have lent S$30 billion to MAS.

– Piyush Gupta, CEO, DBS

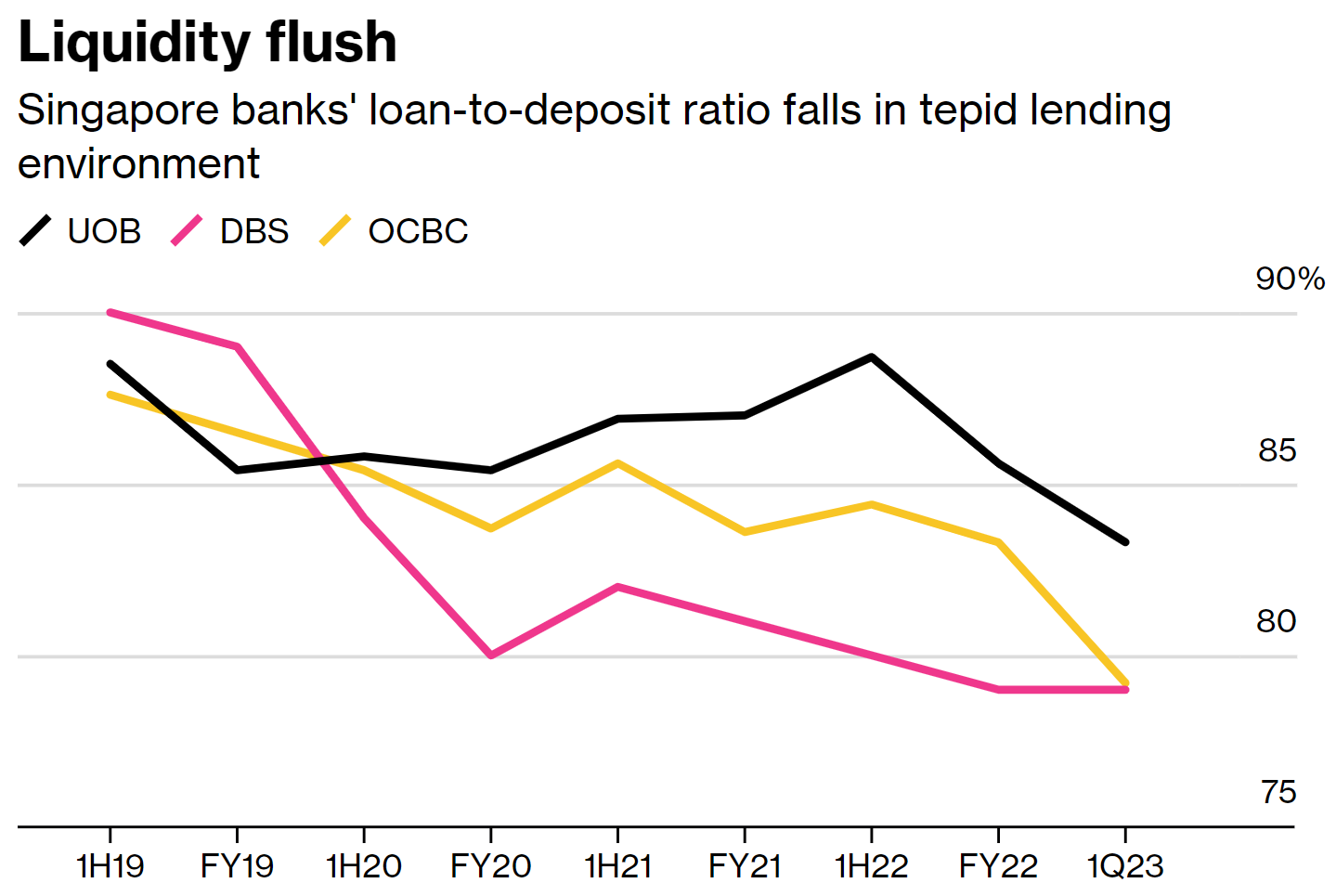

DBS isn’t the only bank afflicted by this “curse of abundance”, as loan-to-deposit ratios have fallen precipitously for all local banks, down from nearly 90 per cent prior to the pandemic, to barely 80 per cent in 2023, driven mainly by international capital and wealthy individuals fleeing to the safety Lion City offers.

Image Credit: Bloomberg

The basic mode of operation of a bank is to take in deposits — in exchange for interest rate payments made to the depositor — and then lend the money out at a higher rate and collect the difference as profit (roughly speaking).

Aside from a small fraction kept in cash for anybody willing to take theirs out, most of the money banks have on their balance sheets is employed somewhere, doing something, yielding a return.

If it doesn’t, it becomes deadweight that earns zero — and zeros in finance are only accepted when they come in a long line, following a positive number at the front.

That’s why “lending” to the central bank by using many of its financial instruments is still a better deal in comparison, though some distance from annual 3+ per cent on mortgages to as much as 27 per cent banks charge credit card holders.

Borrowers rejoice! (sort of)

DBS declined to provide more details about the conditions of the “loan” to MAS when queried by Bloomberg News, but it is clearly a tool of last resort, as more money is made by lending to businesses and individuals.

What it does mean for you, however, is that Singapore is, relatively speaking, one of the best places to get a loan anywhere in the world right now.

With interest rates on mortgages roughly around 3.5 per cent, the city-state compares favourably to most developed countries.

Of course, it’s a far cry from cheap lending of the pre-pandemic era, when global rates were hovering close to zero — and you could buy a property with financing costing you just around one per cent per annum.

That time may not come back soon, though, and three per cent (with some change) still looks mighty attractive compared to about six per cent in Australia and the UK, or over seven per cent in the USA.

Why aren’t loans even cheaper?

If it’s so difficult to put money to work, then you might be wondering why loans aren’t even cheaper.

If banks were able to do as little as one per cent per year as recently as 2021, why can’t they drop their rates now, when they’re struggling to make any return?

There are a few reasons for that, of course:

- The main one is that interest rates in Singapore are not set by MAS, but rather by the free market which is, in turn, dependent on the prevailing interest rate tendencies abroad. That’s why even central bank’s facilities are priced according to those rates, which takes us to the second point…

- Risk. Housing loans are generally more risky than interbank trades or central bank’s facilities (ie. it’s far more likely that a homeowner runs into trouble paying off his debts). So, his loan has to be priced accordingly, above the rates used in the safest transactions. And his ability to repay his obligations is adversely impacted by…

- Inflation – which is really a double whammy. Firstly, it erodes the value of money, that the bank must try to compensate for (each dollar you borrow will be worth less with each year of high inflation). Secondly, it makes the risk of the borrower defaulting on his debt higher (rising prices eat into incomes).

Paradoxically, then, unless we have to endure another period of meagre economic activity, akin to that following the meltdown of 2008/09 (which had kept interest rates very low for over a decade), then we can’t really hope for borrowing to be as cheap as it was then.

It was a great time for Singaporeans, as the country had been doing very well compared to the rest of the world — while reaping the added benefit of cheap borrowing, given how low interest rates were everywhere else.

Now, despite the change for the worse, the Lion City is still in a better situation than almost everybody else is — so much so, that money keeps flooding its shores, overwhelming local financiers who simply don’t know where to put it to profitable use.

And as problems go, this is a good one to have.

Featured Image Credit: Reuters