Covid-19 is keeping everyone at home — and away from ATMs and banks — due to social distancing measures and fear of contracting the virus from common surfaces.

More are turning towards online cash withdrawal services to avoid large crowds.

“It’s only a matter of time that ATMs and bank branches disappear—with or without SOCASH,” said co-founder and CEO Hari Sivan of the online cash withdrawal service in an interview with Vulcan Post.

Pandemic or not, the online startup remains intent on disrupting the cash circulation industry.

Cash Withdrawal Made Easy With An App

Founded in 2015 by Hari and his wife, Rekha, they wanted to allow people to withdraw cash easily from a network of affiliated shops.

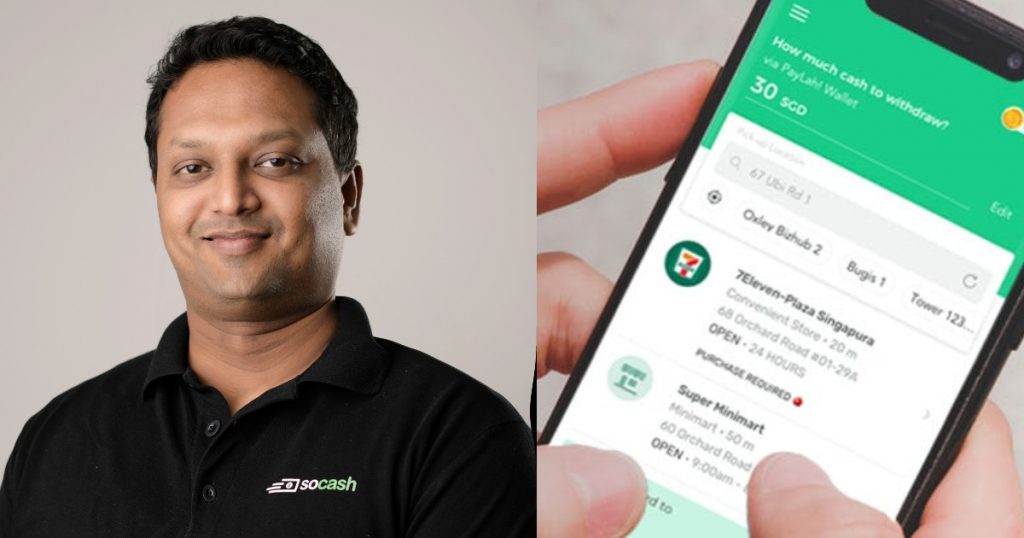

With SOCASH, users can simply download an app on the Apple App Store or Google Play Store and enter the amount of money they need.

After that, they can enter the nearest SOCASH-affiliated shop, scan a QR code and pick up their cash.

With every transaction, users earn points which can be used to redeem rewards, much like the loyalty programme for apps such as Grab.

While SOCASH’s service comes at an opportune time during the Covid-19 pandemic, they have not been immune to the effects of the crisis, which has led to an overall economic recession.

Transaction volumes were down by 35-37 per cent, Hari reported.

To cope with the pandemic, SOCASH “focused on fixed cost reductions, reduced marketing activities and are working on expanding [their] product capabilities to further diversify the revenue streams”.

With that, the startup announced a new partnership earlier this month with Sheng Siong and Prime supermarkets.

SOCASH will be rolling out a new cash machine across 62 branches to reduce large crowds at ATMs and banks and engage in contactless methods for everyone’s overall well-being and safety.

This is a significant departure from SOCASH’s original business model, which relied on person-to-person contact between store merchants and app users to withdraw cash from the counter.

Value-Adding To Banks And Stores

Previously, in a 2018 interview with Vulcan Post, Hari had revealed that banks spent up to US$80 million (S$111 million) in 2015 to maintain ATMs, which hold up to S$400 million worth of uncirculated cash. That’s a tremendous waste of resources.

They’re expensive to maintain, and while it’s hard for banks to operate without them, we see some banks in Asia that are aggressively closing branch operations and removing ATMs.

– Hari Sivan, co-founder and CEO of SOCASH

“The network is breaking down and unable to meet the demand of the next billion starting their consumption journey in Asia,” he added.

By relying on SOCASH merchants instead of expensive ATM cash dispensers, banks reduce costs and gain access to a network of shops that serve as virtual ATMs — a self-scaling last mile network.

SOCASH replicates the ATM/Branch transaction fee revenue model. Banks are SOCASH’s revenue-generating customers, and SOCASH generates revenue with every transaction made in-app that it splits with the stores on its network.

“Our business is primarily driven by the number of transactions, which in turn is driven by the size of our network and the number of banks or financial institutions partnering us.”

SOCASH targets smartphone natives looking for a “small value cash-on-demand,” Hari explains. To date, SOCASH has recorded over 341,000+ downloads for the app.

The drivers impacting user preferences are proximity, privacy and the financially prudent who stays away from credit cards, are sensitive to annual fees and have careful spending habits.

– Hari Sivan, co-founder and CEO of SOCASH

Habit A Barrier To User Adoption

With that, SOCASH remains highly anticipated among banking and investment circles.

The app raised US$5.5 million (S$7.6 million) in a Series A funding round with Vertex Ventures in August 2018.

SOCASH is also the first recipient of the Monetary Authority of Singapore’s Financial Sector Technology and Innovation Grant under the Proof of Concept Scheme.

However, the startup is subject to the same teething issues all new businesses face.

Users continue to rely on ATMs for cash withdrawals, as opposed to making the switch over to SOCASH.

“The reasons range from awareness, proximity, habit & product preferences,” says Hari. “There is a long lead phase of each product co-existing with other payment options.”

Popular blogs reviewing SOCASH have complained about the lack of trained merchants.

Additionally, one of the main incentives to download SOCASH arose from the desire to cash in on the generous reward system—which has since been updated.

“Good things don’t last forever. They were, and probably still are, in what I call “start up phase”, muses The Bulging Wallet, a personal finance blog.

“As you become more mature, your incentives for consumers become less generous — that’s understandable,” it added.

SOCASH is also far from outdoing ATMs in terms of sheer geographical convenience and density.

Currently, SOCASH has over 1,500 withdrawal points across Singapore. By comparison, there are more than 2,050 off-site ATMs, according to a Parliamentary record in 2014.

Statista also reported in a 2018 study that there are 66.45 ATMs per 100,000 people in Singapore.

Turning SOCASH Into The New Global ATM

The solution, then, is obvious: increase the number of withdrawal points, change consumer habits and make every transaction count.

While Covid-19 may have delayed SOCASH’s plans, Hari is bent on seeing the app transit from single-country to multi-country operation.

Currently, SOCASH spans over 16,500+ shops across Singapore, Indonesia and Malaysia. That includes mom-and-pop shops, cafes, retail giants like 7-11 and supermarket chains like Sheng Siong.

According to Hari, the ideal market has a “large digital middle-class population spread over a large geography, does not have high debt-based consumption, has supportive regulators to enable wider access to banking, (and) cost of cash as a significant issue for bank profitability.”

Fortunately, much of Southeast Asia and the greater Asia-Pacific region fit that profile.

Hari also explains that the density of withdrawal points per location will vary depending on the demands of respective communities.

Our goal is to keep cash float to match the daily average demand which is around SGD 15,000 – 25,000 per day for a typical medium-sized residential housing estate in Singapore.

– Hari Sivan, co-founder and CEO of SOCASH

New Features

Apart from increasing the number of stores on the SOCASH network, the app will also be increasing its ease of use and adapting to the Covid-19 pandemic.

Apart from installing cash machines with its merchants to reduce human interaction, SOCASH will also be rolling out QR payment acceptance once regulatory approvals for the ASEAN payment framework is granted.

The startup will then be piloting a sales platform, using shops as virtual branches.

To increase the value add for banks, SOCASH will contribute to the customer acquisition funnel by “setting up distribution of savings accounts, loans, credit cards, etc,” says Hari.

Shifting away from the reliance on reward programmes, SOCASH will be entering its next phase of life and relying on network partners who “have promoted it within their community as local ambassadors.”

Online Cash Withdrawal Services Will Be The Future

Hari sticks to his original caveat that ATMs will become obsolete in the years to come. But it looks like it will be a long time yet before cash becomes obselete.

An international study done by the Bank for International Settlements (BIS) agrees that the “unprecedented public concerns about viral transmission via cash” has led to drops in cash usage in some countries.

But trends differ across cultures, and the same risks exist for card-based payments, which require PIN and signatures. BIS has also expressed that there may be a need to strengthen cash-based transactions.

BIS said, “If cash is not generally accepted as a means of payment, this could open a ‘payments divide’ between those with access to digital payments and those without. This in turn could have an especially severe impact on unbanked and older consumers.”

One thing’s for sure–contactless digital transactions, which companies like SOCASH are moving towards, are becoming increasingly relevant.

For now, SOCASH will focus on refining its product, value-adding to banks, and expanding the network of SOCASH merchants, pandemic or not.

“Our vision is distributed banking,” Hari concludes simply.

The goal? To convert every shop and customer into a virtual cash distribution network starting in Asia.

Featured Image Credit: SOCASH