2020 might commonly be touted as the year for DeFi, but the hype for Stablecoins has long been established in the crypto space.

At Coinhako, we support USD-backed Stablecoins like USDT & USDC, for our Singaporean users to fund their accounts for USD trading with other cryptocurrencies.

In other regional markets that we serve, we provide trading for a wide range of Stablecoins with local currencies for the local market.

So what exactly are stablecoins? How do they differ from other cryptocurrencies? Or what is the perceived value of these assets?

What Are Stablecoins?

Stablecoins are digital assets designed to have a consistent value over time in contrast to the volatility typically seen in cryptocurrency prices.

To achieve this stable value, Stablecoins are “collateralised”— which means that the total number of stablecoins in circulation is backed by assets held in reserve.

The Stable values of Stablecoins have been valuable for crypto traders in times of market volatility to hedge against potential losses and keep profits in fiat value during bear markets, while still being able to hold onto these digital tokens.

The key difference between stablecoins and other tokens is that stablecoins are meant to be non-volatile assets and are backed by assets to safeguard investors.

Supply of stablecoins is also typically set to adjust according to market conditions, and most stablecoins are issued by companies – this even includes commercial banks that have fiat money as the reserve like JP Morgan’s JPM Coin or FAANG companies like Facebook which is working to release its own digital currency known as LIBRA .

Types Of Stablecoins

There are many other ways stablecoins might be collateralised by physical assets; The purpose of them all is to ensure price stability.

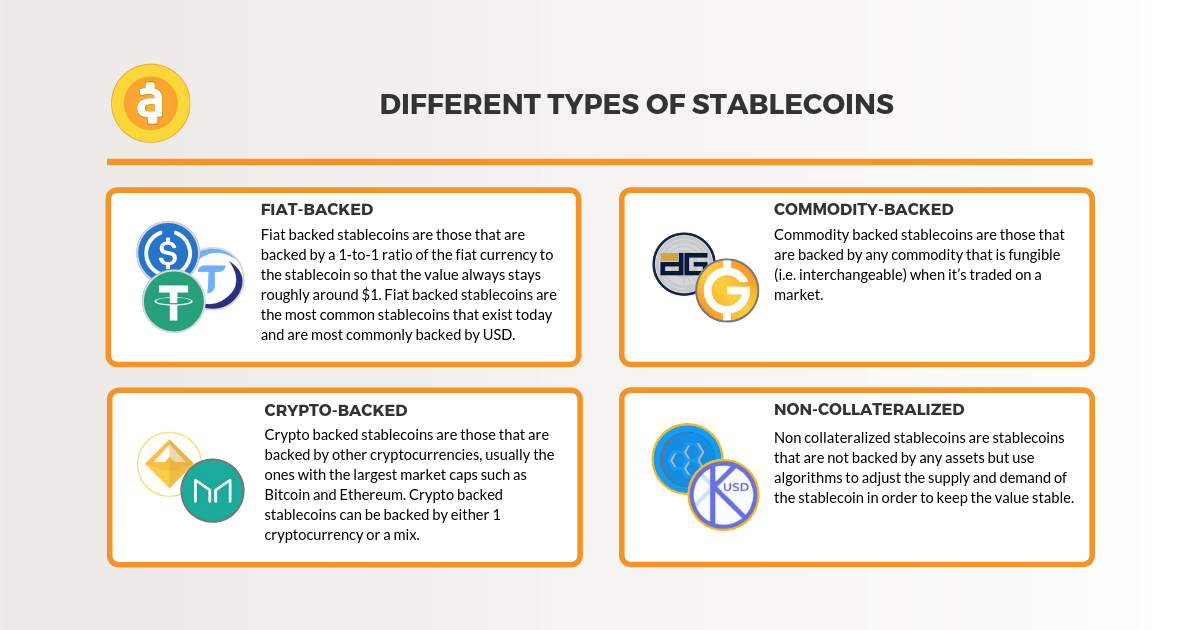

1. Fiat backed stablecoins

Most commonly, stablecoins are backed by fiat currencies such as the US Dollar (USD) which values each token to dollars that are kept safely by a central custodian like a bank.

2. Commodity-backed stablecoins

A commodity collateralised stablecoin functions almost similarly to a fiat collateralised stablecoin. The main difference is that it is backed by some commodities like gold, silver or even a kilogram of bananas.

3. Cryptocurrency-backed stablecoins

Cryptocurrency collateralised stablecoins have specific cryptocurrency in a reserve fund to back the coin. However, due to the volatility of cryptocurrency, the price/earnings to growth ratio (PEG ratio) isn’t 1:1.

4. Non-collateralised stablecoins

Non-collateralised tokens rely on algorithms generated mechanically which are able to change the supply volume to maintain the token’s price. They rely on smart contracts to sell tokens if the price falls below the peg or to supply tokens to the market if the value increases.

How Did Stablecoins Come To Be?

Stablecoins were first issued in 2014. The first two in the scene were BitUSD and NuBits, which were collateralised though other cryptocurrencies instead of fiat assets.

The world’s first stablecoin BitUSD was released on 21 July 2014. This was the product of two future leading figures in the cryptocurrency industry, Dan Larimer (EOS) and Charles Hoskinson (Cardano).

In 2015, RealCoin was introduced and became what is now known as Tether (USDT). Tether is built on the OMNI blockchain and has been a stablecoin market leader since 2015.

Still confused? Here’s a video to help sum up everything we’ve covered so far:

Are Stablecoins Regulated?

Despite being positioned as a “stable” asset class, stablecoins come with a unique set of regulatory concerns.

Combining characteristics of different financial services — stablecoins encompass features of payment systems, bank deposits, foreign currency exchanges, commodities, and collective investment vehicles.

As a result, they pose financial stability risks.

To combat illicit financial activity such as money laundering, regulators in various countries may impose guidelines that require stablecoin trading platforms to implement Know-Your-Customer policies.

Controversies And Concerns Regarding Stablecoin

1. Under-capitalisation

Collateralised stablecoins pose a risk of under-capitalisation, where there is uncertainty surrounding the sufficiency of fiat reserves held to back up the value of the asset.

Because the prices of collateralized stablecoins are pegged against assets held in reserves, controversy arises when it becomes difficult to verify whether these companies actually hold sufficient reserves.

This can happen when companies do not disclose their banking relationships, since that information is required to conduct checks.

2. Price Stability

Though stablecoins are marketed as a stable digital asset, market movements in the past have revealed that stablecoins may not necessarily be immune to high market volatility.

When the cryptoconomy took a plunge in October 2018, Tether dropped below US$1. Earlier in March this year, Tether (USDT) dropped to US $0.96 during a period of high market volatility.

Are Stablecoins Only Issued By Companies?

2020 has also given rise to the hype of Central Bank Digital Currencies (CBDC).

These are digital currencies that are issued by regulators in different countries, mainly made to be pegged to the value of the country’s local currency.

Many countries have given us a peek into their CBDC projects since 2019, and here is a brief round-up of what’s been happening:

A Tokenized Singapore Dollar (SGD)?

Even here in Singapore, our local financial regulator has shared about the development of a tokenized version of the Singapore Dollar (SGD) under Project Ubin – an initiative by the Singaporean government to improve Singapore’s financial ecosystem using blockchain and distributed ledger technology (DLT).

China and the digital Yuan

Shortly after Facebook announced its own digital currency, Libra, the People’s Bank of China announced that it would ramp up the development of its own centralised digital currency.

The purpose of the digital Yuan, according to statements from the central bank’s Digital Currency Research Institute, was to replace some banknotes and coins in circulation, and for small-scale transactions.

France

The Bank of France (Banque de France) launched a series of experiments to pilot its potential central bank digital currency (CBDC) for financial institutions in early 2020. Aimed at ramping up the efficiency of the French financial system and fostering greater trust in the currency, the digital euro pilot sets France on its way to becoming a greater adopter of blockchain technology.

According to French financial publication Les Echos, the digital euro pilot was targeted at private players in the financial sector, and would not be used for retail purposes.

Will the US Dollar be tokenized by the USA?

Plans to tokenize the US Dollar by the USA central bank are already well in discussion.

The proposed Digital Dollar Project was launched in May 2020, and would engage the help of Accenture to launch a digital US Dollar in the United States of America – you can read the Digital Dollar White Paper here.

What’s Next In The Stablecoin Space?

What will the future hold for stablecoins?

While we cannot say for sure what the next milestone in the stablecoin world will be, it is likely that many exciting developments will unravel in the years to come.

With the right regulatory framework in place, stablecoins hold a lot of potential — not only in terms of cryptocurrency trading, but also for filling in the gaps for traditional payment systems worldwide.

This article originally appeared on Coinhako and is republished here with permission.