Once upon a time, instalment plans were associated with buying a house, a car or even a wedding reception, But not anymore.

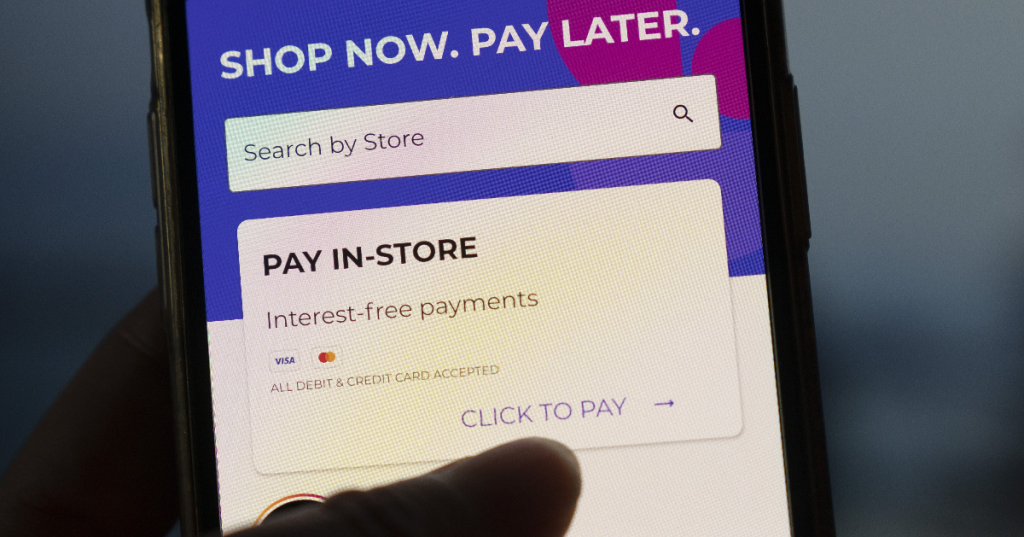

These days, you can literally buy anything and pay for them in interest-free instalments using a Buy Now, Pay Later (BNPL) service. There is no confusion over what it does; the name literally explains it all.

According to a report by FIS, while BNPL still accounts for less than three per cent of all debit and credit transactions today, the figure is expected to grow to 13 per cent by 2024.

So what makes BNPL so popular, and should we be worried?

The growing appeal of BNPL

As far as creating an inclusive society is concerned, BNPL has democratised our financial services.

For the first time, access to unsecured credit is practically available to everyone. Unlike credit cards, there are little to no barriers to entry. Users do not need to earn above a certain income or be subjected to a credit check to ascertain their risk profile. Compared with money lenders, legal or otherwise, there are also no hefty interest rates or guarantors required.

Here lies the magic of BNPL. If the desire to buy things is an itch at an unreachable spot, using a BNPL option is basically getting help to scratch that itch for a serotonin boost.

With the introduction of BNPL, the privilege of instant gratification is now extended to a wider population. Overnight, our ability to make big-ticket purchases will no longer require months of austerity. In fact, clicking “buy” has never been easier since even a low-value item can be split into a negligible number.

But to understand its popularity, we must acknowledge that BNPL services go beyond promoting convenience and flexibility. What it is truly selling is a lifestyle of vapid consumerism. It is empowering, but only at creating imaginary affluence to help us reach our materialistic goals.

So far, BNPL’s meteoric rise boils down to being in the right place at the right time. It is no coincidence that it gained traction during a boom in e-commerce over the pandemic.

And with rising inflation and an imminent GST increase next year, it creates a perfect storm for the demand for BNPL services to surge as consumers struggle to stretch their dollars.

A slippery slope to debt?

It is worth asking – who benefits more from a BNPL arrangement?

Is it the retailers enjoying increased sales and conversion rates? Or is it the consumers who can now buy what they want with fewer financial constraints?

Defenders of BNPL might see it as a more affordable way to finance purchases and free up cash flow. But the thing is, if we cannot afford to buy something, it is practically the market signalling to us that we cannot afford the product just yet. But in an “I want it, and I want it now” culture, saving up for something seems to have become a habit reserved for boomers.

As for freeing up cash flow, what are people doing with that “excess” money that would otherwise be used to pay for the goods in full? Does it end up as savings, or is it used to buy more things?

It is naïve to assume that most users of BNPL will make rational decisions. That they will remain fiscally responsible, not overspend, and only use the service to buy what they need rather than what they want. If that were the case, no one would end up in debt.

BNPL is ultimately a form of debt since we are borrowing against our future to satisfy our current desires. It is also a purchasing model that can get out of control since it lures us into a false sense of affordability.

While the appeal of zero-interest payment plans is the big draw of BNPL services, they are not without additional charges. Admin fees ranging from S$10 to S$15 are imposed for missing repayments.

Considering how nearly half of BNPL purchases are on items that cost S$100 or less, these fees are actually high when seen as a percentage of the value of goods purchased.

Regulating BNPL services

In the wrong hands, BNPL could spiral into a debt trap. While there have been concerns raised in parliament, calling upon the government to regulate the industry to prevent over-indebtedness, it will be a tricky balancing act.

As a financial hub and growing FinTech epicentre, Singapore must allow BNPL firms the space to grow and not be tied down by endless regulations. For now, a BNPL code under the guidance of the MAS has been established to develop a regulatory framework to address the pitfalls of BNPL services.

Meanwhile, BNPL providers also have internal safeguards in place to manage risk. These include spending caps and account suspension, specifically for those who have missed a repayment.

Like everything else, there are pros and cons to using a BNPL service. Used wisely, it can offer us financial freedom. Therefore, self-regulation and restraint, rather than excessive regulations, will be the best protection against the perils of BNPL.

Featured Image Credit: Bloomberg