In the payments industry, two companies reign supreme — Visa and Mastercard. These are the two largest card networks in the world, with cards accepted in more than 200 countries and territories.

They are also some of the largest companies in existence — both Visa and Mastercard are listed within the S&P 500.

However, a look at their recent activity and partnerships might raise some eyebrows. Both companies have been on a partnership spree and many of these companies have something in common: they are cryptocurrency companies.

In October, Mastercard partnered with Paxos for crypto trading, and had previously partnered with Nexo to launch a crypto-backed payment card. They’ve also signed deals with Coinbase, Gemini, BitPay, and many others.

Visa, for its part, has not been idle. Blockchain.com has partnered with Visa to launch a crypto card, as has Crypto.com. Visa also signed a partnership with FTX to offer debit cards in 40 countries, before terminating the partnership in November, in the midst of the FTX meltdown.

For veterans of the payments space, these partnerships seem extremely out of character. Mastercard and Visa executives have shunned crypto in the past, with Visa’s CEO Al Kelly having characterised crypto as a solution in search of a problem.

So why are they now changing their stance and charging towards crypto instead?

Crypto payments represent a real threat to the payments duopoly

When consumers think of payment cards, Visa and Mastercard are probably among the most universally recognised. Retailers partner with them to offer convenience for customers.

For years, they have wielded enormous power, and enjoyed the benefit that this power brings them — Visa and Mastercard reported a net margin of 51 and 46 per cent respectively last year.

Visa and Mastercard charge retailers a fee for the use of their network, which retailers use to collect payments.

But for retailers, there are a host of problems that they have to deal with. Credit card payments, for example, can take a long time to reach merchants, and card companies and banks can take up to three per cent of the transaction value in fees.

Three per cent might seem small, but for retailers, these ‘small amounts’ can quickly add up. By some estimates, it can become retailers’ second-biggest cost after wages.

This is not ideal for retailers. After all, transaction fees cut into profits, and long settlement times mean that the money is locked up until it reaches them.

Yet, without a better alternative, retailers accepted the conditions, and Visa and Mastercard remained at the top of the payments world.

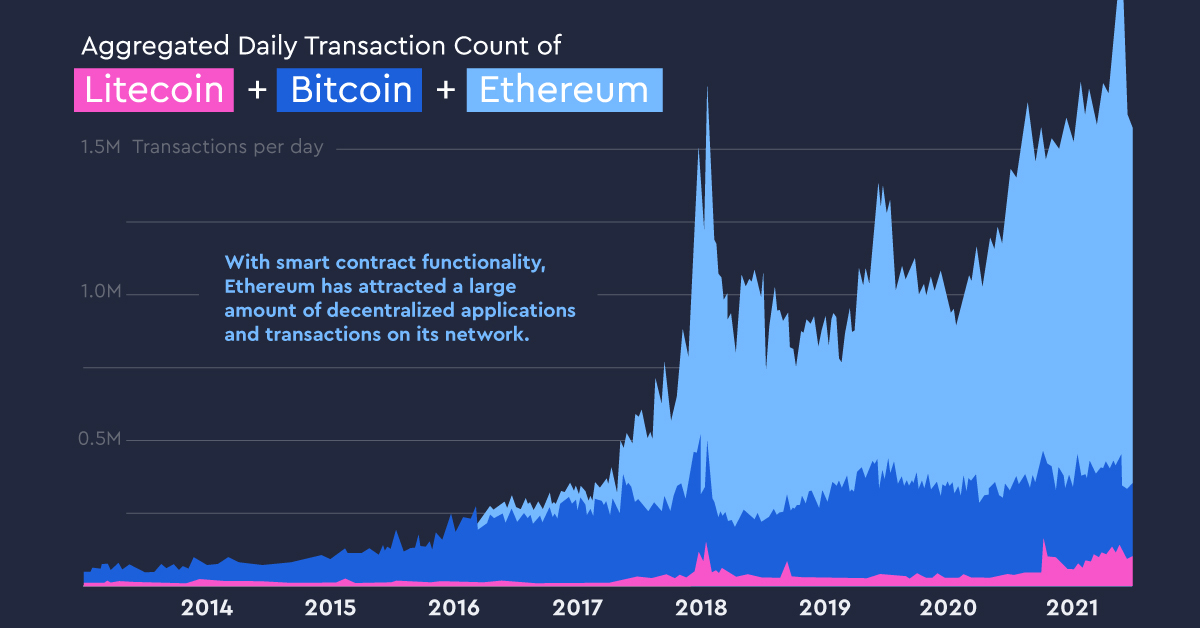

The longstanding payments duopoly, however, is under threat. The rise of fintech, most significantly cryptocurrency payments, presents a real threat to the influence of Visa and Mastercard.

Cryptocurrencies can offer much faster settlement times, and lower transaction fees as well — both pain points that retailers are dealing with. A cryptocurrency like Ethereum can have settlement times as low as 16 seconds, and transaction fees for Bitcoin can be as low as US$1.60.

Crypto payments companies are also building infrastructure to enable crypto payments for merchants and encouraging the use of crypto payments. As such, payments in crypto have been on the rise over the last 10 years.

These developments, of course, have not gone unnoticed by Visa and Mastercard. After all, they stand to lose their position if crypto payments become mainstream. Visa and Mastercard’s golden goose is their network, which thus far has connected consumers and retailers.

The threat of crypto payments is that they do not use this network, and this would mean that the payment giants would be deprived of a significant portion of their revenue.

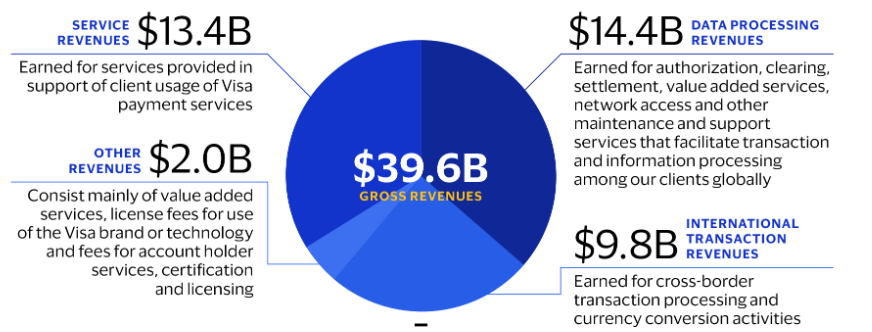

Of the nearly US$40 billion in revenue that Visa earned this year, US$13.4 billion was earned as service revenues and US$9.8 billion was earned as international transaction revenues. This constitutes more than half of their revenue, and does not even include other services such as authorisation, clearing, and settlement.

With crypto payments companies offering something that could bypass them as a middleman, Visa and Mastercard would be foolish to simply sit by and allow their empires to crumble.

If you can’t beat them, join them

In his book Destined for War, political scientist Graham Allison used the term ‘Thucidides Trap’ to describe a situation in which a rising power is threatening to displace an existing one.

The result is that the existing power fears displacement, and war ensues as the existing power attempts to crush the threat to its position. After all, if it does nothing, the rising power will eventually eclipse it. Therefore, the best course of action is to act decisively now, while it still has the upper hand.

While the term is used to refer to countries and governments in explaining why war exists, its lessons hold true in business as well.

With the rise of crypto payments threatening to displace Visa and Mastercard, the payments giants are facing such a situation. If they do nothing, they will eventually have to concede a large portion of their power.

Given such a situation, the partnerships that they are making seem a lot more sensible. Instead of fighting the crypto payments space, they are expanding their reach, and trying to become the middleman for crypto payments.

After all, if crypto payments continue to use the Visa and Mastercard network, the crypto payments industry will become a far smaller threat. Instead of allowing crypto companies to overtake them, the payments duopoly is co-opting the nascent industry to maintain their preeminent position within the payments industry.

The great strategist Sun Tzu would applaud this move. In the Art of War, he advises against direct confrontation as a means to achieve victory, and instead emphasises the need to achieve victory through other means. Victory through battle is costly, and should be avoided. Instead, he advises generals to seek victory without battle.

Visa and Mastercard have taken this advice to heart, and are avoiding a head-on confrontation with the rising crypto payments industry. Instead, they are cooperating with crypto companies in order to ensure that their position within the payments industry remains on solid ground.

This may not be a bad deal in itself. In fact, in many ways, this is a win-win for both the payments duopoly and the growing crypto payments industry.

Visa and Mastercard already have the infrastructure needed to support crypto payments, and their network is indeed valuable for businesses. The value proposition of Visa and Mastercard has not changed — they still offer companies the chance to reach more customers and simplify the payments process.

For Visa and Mastercard, this cooperation can help to keep them in the game. Instead of having to fight off a competitor, they can continue to enjoy the profits from providing access to a new group of customers, namely, holders of cryptocurrencies.

Is crypto ready to welcome the payments giants?

If the reaction of companies like Crypto.com and Paxos are anything to go by, crypto companies are more than happy to welcome Mastercard and Visa.

When Crypto.com announced its global partnership with Visa, they cited several benefits that the partnership brought for them. The partnership would advance Crypto.com’s ambition to accelerate the adoption of crypto payment solutions around the world, and expand Crypto.com’s reach into new markets and new customer segments that Crypto.com did not yet serve.

According to Visa, crypto companies are the ones lining up to knock on Visa’s door, not the other way round. After all, these partnerships make crypto more visible and provide some legitimacy for crypto companies that manage to secure such partnerships.

Yet, while companies are free to make their own decisions, they are not free from the consequences of these decisions.

For starters, not all cryptocurrencies may be welcomed by payments giants.

Since these payment giants derive revenue from the quantity and size of payments, cryptocurrencies with large block sizes to facilitate large numbers of transactions will be favoured for their ability to facilitate such payments.

For cryptocurrencies with such properties that are not endorsed by Visa or Mastercard, they may find it increasingly difficult to compete with the legitimacy and networks of these payment giants.

And for those that are endorsed by the payments giants, the risk is that they become reliant on the networks that these payments giants provide, and eventually, cease to provide some of the benefits that crypto payments promised at the start.

After all, if Visa and Mastercard continue to take their fees as a percentage of transaction values, retailers may simply end up with additional fees to account for as they pay more middlemen.

Therefore, the benefits of using blockchain technology and cryptocurrency for payments settlements may simply accrue to payments companies like Visa and Mastercard, with consumers and retailers seeing only a small portion of the benefits that crypto payments can bring.

The payments duopoly, with its current network and utility, can indeed provide the nascent crypto payments industry with plenty of benefits — accelerating mass adoption through legitimation and scalable solutions.

But at the same time, the arrival of these payments giants on the crypto payments scene may also mean that an eventual victory by the crypto payments industry over the old Web 2.0 payments industry that birthed Visa and Mastercard may not be a complete one, especially if Visa and Mastercard continue to function as important middlemen within the payments industry.

So will the payments duopoly be broken by crypto payments? Probably not, considering how Visa and Mastercard are already moving to partner with crypto payment firms.

Barring the rise of a Web 3 version of Visa or Mastercard, the crypto payments industry is headed towards reliance on the old payments giants, though this is not exactly a bad thing in itself.

Featured Image Credit: PYMNTS.com