Disclaimer: Opinions expressed below belong solely to the author.

Founded in 2012, Grab was once the darling of Singapore startups and is now touted as a ride-hailing giant.

Over the years, it has expanded across different verticals — from delivery, to booking services, and even financial services — and the Southeast Asia region. Aside from Brunei and Laos, Grab operates in all ASEAN countries.

Yet, the company seems to be past its peak. Ever since the company went public with an IPO, its share price has tumbled more than 60 per cent. The company has had to continuously assure investors that it has plans to make itself profitable over the next few years, most recently at its first investor day yesterday.

What’s behind Grab’s troubles? How has a tech giant like Grab managed to dig a hole this deep, and can the company actually deliver on its promise to make itself profitable?

Is ‘growth at all costs’ a viable strategy?

First of all, we should recognise that Grab does indeed have quite a bit going for it. It is a company that is constantly releasing new products and features for its customers.

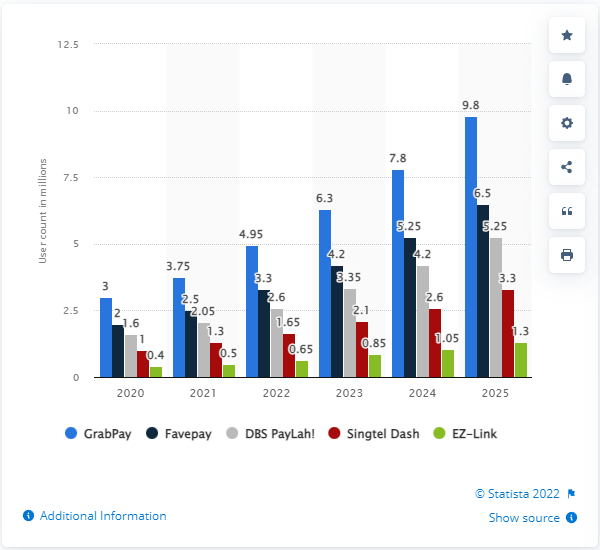

Several years ago, they developed and launched GrabPay, an e-wallet that allows users to store money and pay for goods and services on the Grab platform.

Beyond this, Grab has also launched its own mapping and location service known as GrabMaps, scholarships known as GrabScholar, financial services under GrabFin, and digital bank GXS in collaboration with Singtel.

Needless to say, this is quite the portfolio for a company that originally started with the vision of making taxi rides safer in Malaysia.

But this is also a reason for its consistent inability to turn a profit. All new ventures require capital, and for a company that wants to build everything like Grab, this necessitates large amounts of capital — whether this comes from profitable arms of its business, or from new capital being injected to the company through fundraising rounds.

Throughout the past decade, this has never really been a problem. Investors believed in the growth-at-all-costs model, and Grab’s dominant position gave investors the confidence that they needed to invest.

But what goes up must come down — and when investors began to tighten their belts and take a closer look at how profitable their investments were, Grab’s position and strategy became untenable.

The mentality turned from funding growth-at-all-cost strategies to looking for companies that had a clear path to profitability, and this is where Grab was caught off guard. To shift strategies is in itself, a significant change.

Such transition is not something that companies on stable footing should fear. Companies like Amazon have not recorded huge profits precisely because they have continuously reinvested revenue from profitable arms of their business into newer and loss-making arms to help them overcome any barriers to entry and profit in the future.

Yet, Amazon has consistently grown throughout its history — it’s now one of the FAANG stocks that many investors look at. So to suggest that this strategy is inherently a failing one is probably not accurate.

At the same time, this comparison also raises the question: if both are doing the same thing, why has Amazon managed to turn profits, no matter how small?

While it’s not exactly an apple-to-apple comparison, the question still deserves some answering; and we can look no further than Indonesian unicorn Gojek (or GoTo) for a good comparison.

Strategy is not to blame, but tactics are

Like Grab, Gojek was a ride-hailing startup, albeit with a slightly longer history. While Grab was founded in 2012, Gojek was founded in 2009.

Similar to its Singaporean counterpart, Gojek has its fair share of mergers and acquisitions. It merged with e-commerce startup Tokopedia to form GoTo, and like Grab, it also operated with the growth-at-all-costs strategy until recently.

Given their similarity, both companies have been fierce competitors in the shared space of ride-hailing, food delivery, and more. But as of last month, it was reported that “GoTo has fallen less than its competitor and its market value of about US$26 billion is now twice that of its Singaporean peer.”

There are differences in the way that GoTo and Grab go about their expansions, and this is the key to the differences in their performance.

Grab’s approach to expansion has been characterised by relentless spending — it built its own payments system in GrabPay, and now, its own mapping and location services with GrabMaps.

While GrabPay has seen some success with many using the service, the same cannot be said for GrabMaps.

Complaints abound when it comes to the accuracy of their maps, and for an app that relies on delivery riders and drivers, having accurate maps is of the utmost importance. Would it not have made more sense to partner with an existing map provider, rather than building one by itself?

On top of this, Grab also bought out Uber’s operations in Southeast Asia several years back. Lest we believe that this was a one-off expense, Grab has also acquired several other startups over the years, including Move It, a motorcycle taxi service in the Philippines, Jaya Grocer, a supermarket, and OVO, a digital payment startup.

These acquisitions are market share acquisitions, intended to bolster Grab’s hold on certain markets where they face competition.

Additionally, Grab shifted its core business to deliveries during COVID, which outperformed its ride-hailing services. While this may have been a move that helped Grab through the pandemic, its reliability as a pillar of continued growth is another question.

Contrast this with Gojek. The company merged with e-commerce startup Tokopedia to form GoTo — and instead of building something that capitalised on the pandemic, it utilised a strategy that would keep the company evergreen by doing things well.

It should come as no surprise that with the pandemic winding down, Grab’s performance is also waning.

At last week’s Tech in Asia conference, GoTo co-founder Kevin Aluwi was invited to speak on the company’s path from a startup to a unicorn, and he summed up his company’s struggle: “One of the things that is very dangerous during bull markets is using money to buy growth.”

Characterising Gojek as a chronically underfunded startup, Aluwi suggested that this restriction forced the team to be innovative with their solutions and conservative with their spending.

At the end of the day, the coup de grace of the growth at all costs strategy remains the product — and Grab seems to have missed out on this due to its relentless spending on varied interests that offer little for its customer and user base.

Monopolies and market domination are revenue generators for sure, but lasting monopolies must be guarded by products that are difficult to displace.

At the end of the day, does size matter?

Of course, it cannot be denied that Gojek started with a considerable advantage in terms of market size.

Indonesia is the world’s fourth-most populous country in the world, meaning a larger market size to expand into. In contrast, Singapore and Malaysia — with a combined population of around 40 million — have a mere seventh of Indonesia’s 275 million.

And for Indonesians, Gojek is by far the preferred choice for ride-hailing, food delivery, and much more. This is an advantage that is difficult to overcome. After all, a customer base is not something that can be grown by simply throwing money at it.

But, once again, the obstacle is not insurmountable. Grab’s history of expanding into new markets proves as much. The journey of a small startup to a decacorn that operates throughout most of Southeast Asia is still quite a remarkable one.

While throwing money at Grab to expand into other markets and increasing their total addressable markets may not work, it is not too late for Grab to double down on what helped them expand in the first place — offering customers and users something of value.

The sheer number of customers that Grab has provides a huge sample size for testing new features, offerings, and services — perhaps services that Grab can count on to turn a profit in the future.

Grab has spent much of its cash and time obtaining significant market shares in Southeast Asia, whether it is ride-hailing, deliveries, or financial services. The time has now come to capitalise on this dominance — with better services, improved product offerings, and more.

While this may indeed necessitate more spending, it is different from Grab’s spending over the past decade.

Instead of acquiring competitors, perhaps it is time that Grab become the competitor to beat, and become a true tech giant of Southeast Asia. Its strategies so far have only paid off partially, and to keep trying the same thing while expecting different results is the definition of insanity.

In the meantime, Grab, and other companies like it, should take note of the lessons that Grab has had to learn the hard way.

Firstly, throwing money at problems does not necessarily mean that the problem gets solved. Like all resources, money is not unlimited. It must be spent wisely and conservatively, or one ends up spending unnecessarily.

Secondly, dominance is not an end in itself — it is a means for further domination and the solidification of one’s position in the market. Grab, while expanding to more markets, has not necessarily used this advantage well.

Finally, one should not confuse short-term fixes with long-term solutions. Grab’s success during the pandemic with food deliveries is something laudable — it demonstrates the company’s adaptability to new circumstances, but its scramble to adapt to the new paradigm of sustainable development is also worrying for investors.

As of now, Grab still has an advantage in several aspects. Its market dominance in Southeast Asia is mostly unmatched, and it is still known for the innovations that it brings to the region with its services. But this reputation is declining in the face of investors’ demands to demonstrate sustainable growth and profitability.

While only time will tell if Grab can pull itself out of this slump, the story of Grab’s rise and its stumble should provide valuable lessons for companies, including Grab itself.

Featured Image Credit: Nikkei Asia